Claiming Superannuation TPD Payouts

If you cannot work again due to an injury or illness, you may be eligible to claim a total permanent disability (TPD) payout through your superannuation fund insurance. Your condition could be a mental illness, a chronic sickness or medical issue, or a physical injury.

The lump sum superannuation disability payout is a valuable financial resource to support your lifestyle when you are unable to earn an income. Many Aussies are unaware they:

- Have disability insurance with their superannuation provider

- Of their eligibility to make a TPD claim

- How the TPD claims process works

- The steps to ensure they maximise their TPD insurance benefits.

To help you make the most of your entitlements, we created the Ultimate Guide to TPD Payouts through superannuation funds. This guide will show you how to have a successful claim and ensure you receive what you are owed when you can no longer work.

What is a Superannuation Insurance Payout?

First, let’s define a superannuation insurance payout. As an Australian worker, your employer must deposit funds into your super fund account to help support your retirement lifestyle.

Your superannuation account includes several disability insurance policies, like income protection, terminal illness or life insurance, and TPD insurance.

When the unexpected happens, and you can’t work in your regular occupation anymore, you could claim against one or more of these insurance policies. If you have more than one superannuation account, you might be eligible to make multiple TPD claims.

When you have a successful TPD claim, a lump sum payout will be deposited in your superannuation fund account, where you can either:

- Withdraw the whole amount.

- Withdraw some of your payout.

- Leave it in your super account until you reach retirement age.

How Much is the Average TPD Payout Amount?

In Australia, the value of average TPD payouts ranges between $30,000 and $50,000, with most being above $200,000, and some fortunate people receiving up to $1.5 million. Your superannuation fund insurance terms and conditions will determine how much you receive for a total permanent disability insurance payout, which can vary significantly. Generally, the specifics of your case, such as:

- The nature of your injuries

- Your pre-injury employment

- The length of time you have been unable to work will also play a factor.

A total and permanent disability (TPD) claim payout can significantly help the financial situation of people and their families who are coping with a severe illness, injury or mental disorder.

Can I Claim Multiple TPD Payouts?

Many Aussies have more than one superannuation fund due to job hopping. Because of this, they have more than one disability insurance policy, enabling them to claim multiple benefits that can be worth millions. However, each TPD claim is individually assessed, so some could be accepted while others fail.

To learn if you can receive more than one TPD benefit payment, contact our friendly legal team for a free case review. Call 1300 873 252 or email us

How much do lawyers change for TPD claims?

Who is Eligible for a TPD Payout?

To be eligible for a TPD benefit payment, you must have Total and Permanent Disability (TPD) Insurance as part of your Superannuation policy (or independently of your superannuation) on the day you last worked or became permanently and completely unable to do your job (or one for which you have training or experience).

You can find out if you are eligible by checking your superannuation policy statement or calling your super fund with your TPD policy questions, ensuring you get the answers in writing. Check if you had TPD insurance cover when you ceased work, as your super provider could tell you otherwise when you call.

If Aussie Injury Lawyers is managing your case, it’s free for us to review your insurance coverage and explain your legal options. To know if you can make one or more TPD insurance claims, call us now on 1300 873 252

What Percentage of TPD Insurance Claims Get a Payout?

What percentage of TPD insurance claims get a payout? Fortunately, the Australian superannuation research firm SuperRatings has published data regarding the percentage of successful TPD insurance payouts. According to their research, when you lodge a properly prepared disability claim that correctly addresses the TPD definition in your policy terms, you can feel confident about receiving a lump sum payout.

Their statistics show that between 71% and 100% of such claims are successful, meaning up to 30% of people miss out. Also, a significant number did not receive the full value of their entitlements.

Regarding TPD claim rejections, Australian Securities and Investments Commission data puts the insurance industry average for denied permanent disability claims at 16%.

You will be pleased to learn that Aussie Injury Lawyers has a 99% TPD claim success rate. Our skilled superannuation insurance lawyers have helped thousands of everyday Australians access all their due superannuation benefits. Choose the law firm that specialises in just one area of law – superannuation insurance claims, when you want to win your TPD payout – Call 1300 873 252

How much is my TPD Payment worth?

Can I Make Multiple Claims if I Have More Than One TPD Insurance Policy?

Yes, you can! If you have multiple insurance policies or have TPD insurance included as a part of your superannuation funds, you can claim multiple disability benefits for one physical injury, illness or psychological disorder as long as it meets the TPD definition of each TPD policy.

Multiple TPD claims are possible because each separate insurance policy operates independently from the other and may even cover only specific benefits. Claiming against multiple TPD insurance policies will involve additional claim forms and effort, but will be worthwhile, particularly if you are concerned about relying on a single insurance policy. Making more than one claim increases the chance of winning at least one (or more than one), giving you funds for medical costs and other expenses.

Use our free online check to see if you can claim >

What Are the Most Common TPD Payouts?

You can successfully claim a TPD insurance payout under a range of circumstances. The most common types are:

Workplace Injury TPD Claims

If you have suffered permanent impairment because of a work injury and can no longer work in your regular occupation, you could make a superannuation claim. You could also claim workers’ compensation and, when approved, receive weekly payments and a one-off lump sum payment.

Non-Work Related TPD Claims

When you suffer a physical or psychological injury independent of your job (and you can no longer work), you could have a successful claim. For example, you had a car accident while on vacation, and your damage is permanent or long-term.

Serious Illness Claims

When you have been diagnosed with a serious or terminal illness like cancer, dementia, stroke or heart disease that stops you from working, you could win your TPD benefit. Success will depend on how long you have been absent from work and whether or not there is a chance your condition will improve enough for you to return in the future.

Infectious Disease TPD Claims

Whether treatable or not, infectious diseases are a leading source of TPD claims. Diseases like HIV/AIDS, TB, and malaria, can make people too sick to work.

Can I Get a TPD Payout for a Mental Illness?

You can claim TPD for a mental health condition, as this can be considered a total and permanent disability, similar to a physical injury. However, the process of accessing disability benefits for a psychological illness or psychiatric disorder can be more challenging. Proving your level of disability is made more accessible when you are receiving regular therapy from a mental health professional who is documenting your treatment.

Some commonly recognised disorders that qualify for mental illness TPD payouts include:

· Depression

· Bipolar disorder

· Schizophrenia

· Post-traumatic stress disorder

· Obsessive-compulsive disorder

More about mental illness TPD claims

What are the Requirements to Lodge a TPD Claim?

These are the standard requirements for lodging a TPD claim with most insurance companies.

- You must have a persistent or long-term physical or mental disability that stops you from earning an income in your regular profession.

- Before submitting a claim, you must wait for the time period specified in your policy or fund’s terms. The waiting period is between the start of your permanent impairment and lodging your TPD insurance claim.

- Medical evidence, such as reports and assessments from your treating doctors or independent evaluations, must support the severity of your medical condition and its impact on your work capacity.

- You must meet the TPD criteria outlined in your policy terms and conditions.

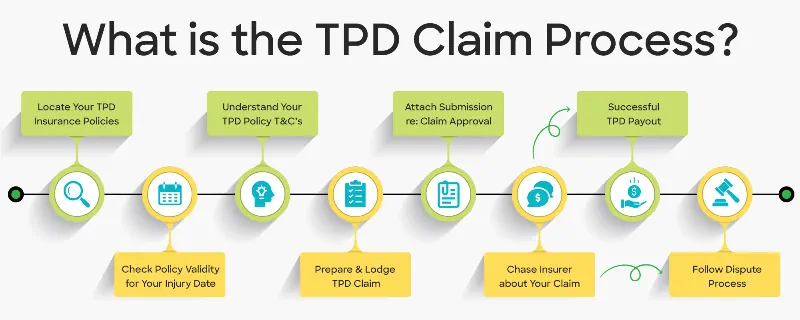

What is the Claim Process for a TPD Lump Sum Payment?

The process for a permanent disability insurance claim involves several steps that can differ depending on the requirements of the super fund insurer. However, these are the general guidelines.

Confirm Your TPD Insurance Cover

First, locate all your total and permanent disability (TPD) insurance policies, which may be held through a superannuation fund or as standalone policies. Then check the insured benefit amount and the TPD definition for each policy.

Gather Medical Evidence

You will need compelling evidence for a successful TPD payout, like your medical history, expert reports, and an independent medical assessment that shows how your injury or illness prevents you from working.

Lodge a Complete and Accurate Claim Form

Next, fill out and lodge a TPD claim form with your insurer. This form must be accurate and complete, including all relevant supporting documentation.

Attach a Persuasive Claim Letter

Along with your claim form, you should include a detailed submission letter explaining why you meet the TPD definition under your policy.

Claim Assessment by the Insurer and Super Trustee

The insurance company will review your claim to determine if you meet the TPD criteria, which may involve requests for further information. Once approved, the superannuation fund trustee will also conduct their own review before releasing the lump sum payment into your superannuation account.

Receiving a TPD Lump Sum Payment

Once approved, the lump sum payment will be deposited into your superannuation account. From there, you can choose to withdraw the funds, leave them invested, or transfer part of the payout according to your financial needs.

Seek Expert Legal Advice

We highly recommend seeking expert advice from experienced TPD lawyers or financial advisors during this process. They can help prepare your claim effectively and ensure you meet complex policy definitions so you receive maximum compensation.

Is it Difficult to Claim a TPD Insurance Payout?

A total and permanent disability payout is an insurance claim, so success relies on your capacity to meet (or exceed) the TPD definition in your policy terms.

Many Aussies find it too hard to satisfy their insurer’s requirements, so they give up. They tried to claim their payout by simply filling out a few forms without knowing how to create a compelling case. For this reason, insurance companies enjoy people managing their cases (instead of using expert TPD lawyers), as they can minimise or deny claims more often.

Make the best financial decision for your future and rely on our 99% TPD Payout success rate to be certain of maximising your entitlements. Aussie Injury Lawyers is a 100% no win, no fee law firm, which means you only pay fees when you win and nothing if you lose. You carry no financial risk.

It’s free to know the value of your claim and your chance of having a winning payout. Contact our skilled compensation lawyers by calling 1300 873 252 to get started now.

What to Do About Denied Superannuation Insurance Claims

Don’t give up hope if you make a TPD claim and are denied a TPD benefit. There are several reasons why a TPD claim can be refused, including:

· Inadequate medical evidence

· Not meeting the definition of permanent disability

However, just because you receive an initial rejection doesn’t mean it’s the end of the road. You can appeal by providing more comprehensive medical evidence or seeking legal advice to understand your rights and options.

While a successful TPD claim may be difficult to achieve, you can still receive the full TPD insurance benefit and the payout you deserve with the right approach and support.

More about rejected TPD claims

What is the Time Frame for a TPD Payout?

Most people with a valid claim want to know the timeframe for a TPD Payout. You will receive a lump sum payment within 6 to 12 months of lodgement. Of course, some cases take longer, particularly for large superannuation disability payouts or complex claims.

Typically, the insurance company will complete their assessment within 6 months; however, there is another review by your superannuation trustee. This stage is usually completed within 1 to 2 months.

The primary cause of late claim payouts is incomplete or inaccurate assessments or submissions. Should you lodge a dodgy application, you will experience a long process of multiple information requests and waiting for each response. Insurance companies rely on applicants abandoning the TPD claim process as it becomes too challenging.

How Do I Fast-Track a Permanent Disability TPD Insurance Claim?

Lodge an Accurate Claim: Providing sufficient and compelling evidence to support a TPD claim can fast-track the process, as incomplete submissions will result in the insurer requesting additional information (multiple times), prolonging the TPD claims process.

Write a persuasive letter explaining why you should receive your payout; failing to do so often leads to claim rejection.

Please follow up with the insurance company to confirm they have all the required information; a hands-on approach will expedite your claim payout.

Aussie Injury Lawyers‘ has a team of TPD payout specialists with a comprehensive understanding of the claims process, including the factors that make insurers delay payment. Be certain of accessing your payout when you need it most by contacting us now for free TPD claim advice – Call 1300 873 252

How Do I Receive TPD Lump Sum Payout?

Once approved, you receive either a monthly income payment or a lump sum payout deposited into your superannuation account, giving you the following options:

- Withdraw the funds

- Transfer part of your payout into another account.

- Keep the funds in your super account for retirement.

When you receive your payment, it is recommended that you seek expert financial advice. Your choices will impact how much tax you pay, with some options being tax-free.

Next, our ultimate TPD payout guide reviews the tax implications for lump sum payouts.

What is the Tax on a TPD Payout?

Your lump sum TPD payout is not considered taxable income unless you withdraw all or part of these funds from your superannuation account. You will owe “superannuation lump sum withdrawal tax” when you do this. Here are the factors you must consider:

- Taxpayers aged 60 or over are exempt from tax on TPD benefit payment.

- If you leave your TPD payout in your super account until retirement age, it is tax-free.

- The TPD tax calculation for people under 60 is based on their age, eligible service date, and the date they joined a superannuation fund.

- When you are below your preservation age, some withdrawals are tax-free, and the balance is taxed at 22%.

- People who have met their preservation age but are below 60 years old are eligible to withdraw a maximum of $225,000 free from taxes.

- When withdrawing over $225,000, a portion of the withdrawal amount is tax-free, and the remaining taxable portion is subject to a 22% tax rate.

The other frequent question about TPD payments is, how will it change my Centrelink payments? We examine that next.

More about tax on TPD payments

About a TPD Payout and Centrelink Payments

Does a TPD payout affect Centrelink entitlements? This is a common question for those about to claim TPD.

So, it’s reassuring to know that when your TPD payout is deposited into your superannuation account, it does not impact your Centrelink payments (when you leave it there). Centrelink does not include your superannuation account balance in its means test until you qualify for the age pension, which is generally around 65 to 67 years old; generally, receiving a TPD payout does not affect other benefits, including child support payments and the Centrelink disability support pension.

However, your Centrelink payments will likely change when you remove money from your TPD payout or superannuation account. For this reason, we recommend seeking advice from a qualified financial advisor before deciding to move funds.

Can I Return to Work Following a TPD Payout?

In some circumstances, you can return to work following a TPD payout. Whether or not you can work again depends on your insurance policy terms and conditions and other factors.

Most TPD insurance policies fall into one of these two categories:

- Can’t return to work in your occupation

- Can’t return to work in any occupation

The first category means you are unfit for your regular job or any other occupation aligned with your existing training and experience. This means that after receiving a TPD payment, you could train to work in a different industry and return to work.

For example, you used to work as a bricklayer doing hard manual labour, and your medical condition prevents you from doing this job or any other manual labour work. After a TPD payout, you could study at a college or university and then work in a profession where you sit behind a desk to do your job.

The second category is more challenging. When your policy says you can’t work in any occupation, you cannot return to your usual job or any other occupation. The exception is when a new treatment or therapy helps you recover from your ailment to the point where you can work again. In this situation, you could potentially return to work and retain your total and permanent disability payment.

Please ensure you receive expert legal advice before making any decision regarding going back to work.

More about working after a TPD payout

How Our TPD Payout Lawyers Can Help

A successful TPD payout provides financial security and stability for you and your loved ones when you have a permanent or long-lasting disability. These payments are often tax-free, and in some cases, you can return to work following a TPD compensation payment. Certain mental illnesses also qualify for a payout.

Our experienced TPD Lawyers will evaluate your case for free. We provide expert legal advice, guiding you through the claims process to a winning outcome. As part of our comprehensive claim review, we will:

- Locate your valid TPD insurance policies.

- Closely examine the fine print.

- Understand the applicable TPD definition.

- Let you know how many claims you might have.

- The value of your claim.

- How likely you are to succeed.

- Your recommended steps to securing your lump sum payout.

You will have peace of mind knowing Aussie Injury Lawyers win 99% of disability insurance claims. Rely on our knowledge and expertise to get the most out of your TPD insurance cover. There are no upfront costs, and our “100% no win, no fee” policy ensures you pay nothing if you don’t win.

Total Permanent Disability Insurance Payout FAQs

How much do you get for a TPD claim in Australia?

In Australia, TPD payout amounts range from $30,000 to $50,000, depending on the value of TPD insurance cover. Those eligible for multiple claims can claim multiple TPD benefits, often worth millions.

How is TPD paid out for a successful claim?

When you have an approved claim, a TPD benefit is paid into your super fund account. You generally won’t pay tax on these funds when you leave them there until you reach retirement age. However, there will be tax payable if you make a withdrawal before reaching your preservation age, but likely at a lower tax rate.

Does a TPD payout come out of your super account?

A TPD payment is not taken from your super account. Instead, these funds come from an insurance policy payout when you win an insurance claim. Many working Aussies have default TPD cover through a super fund.

How long is an average TPD claim?

The time to make a TPD claim and get a lump sum payment typically ranges between six and twelve months, with complex cases taking longer.

How does TPD work in Super?

TPD insurance is a vital source of financial support when a total permanent disability stops you from working. When approved, you receive a one-off TPD benefit payment to help maintain your lifestyle and pay medical expenses. Sadly, many employees are unaware that they have TPD cover through their super fund.